Employer-paid healthcare costs will rise sharply in 2026, further squeezing corporate profits already squeezed by rising labor and operating expenses.

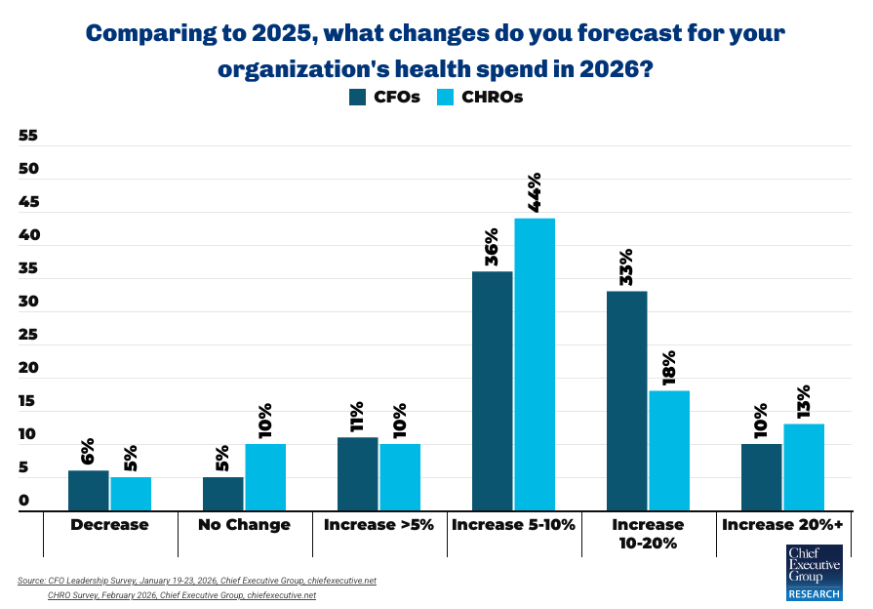

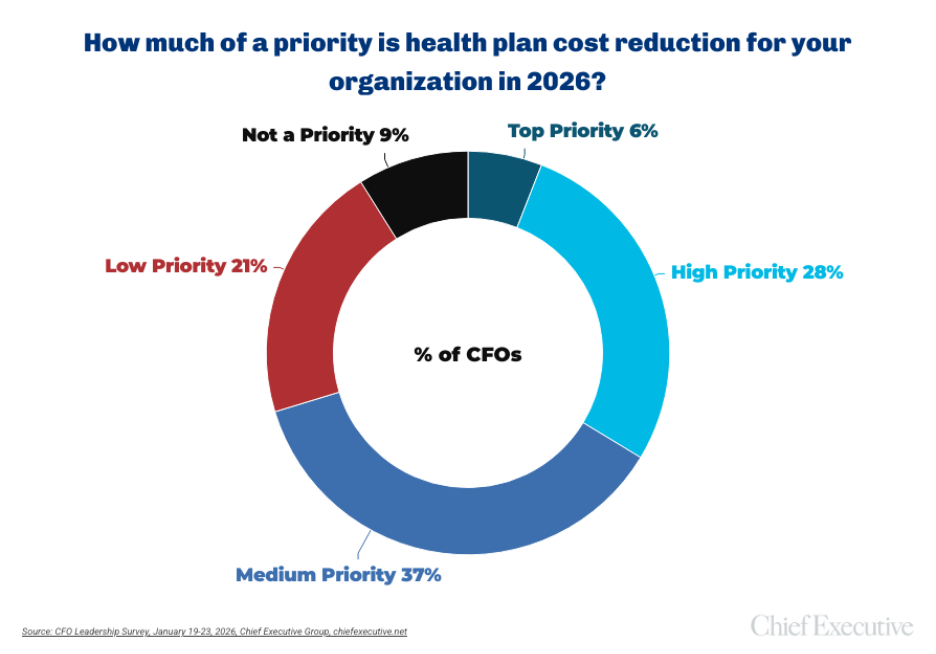

However, despite 9 in 10 reporting premium increases and 43% expecting premium increases to be in the double digits, only 6% of CFOs surveyed by CFO Leadership in January said lowering health care costs was their organization's top priority.

CHROs report similar pressures, with 85% saying per-employee healthcare costs will increase in 2026, and about a third citing an increase of more than 10%.

This outlook echoes the sentiment of CEOs: 81% told our sister publication chief executive As of February, medical costs were expected to increase this year, with 43% expecting an increase of more than 10%.

Healthcare remains one of the largest operating cost categories for U.S. employers. According to Aon's 2025 survey data, employers subsidize about 80% of the total premiums for employer-sponsored plans, and employees pay the rest.

One human resources manager said, “20% year-over-year insurance premium increases are unsustainable,'' and other human resources managers echoed this sentiment.

However, this research suggests that many companies feel constrained in their ability to act.

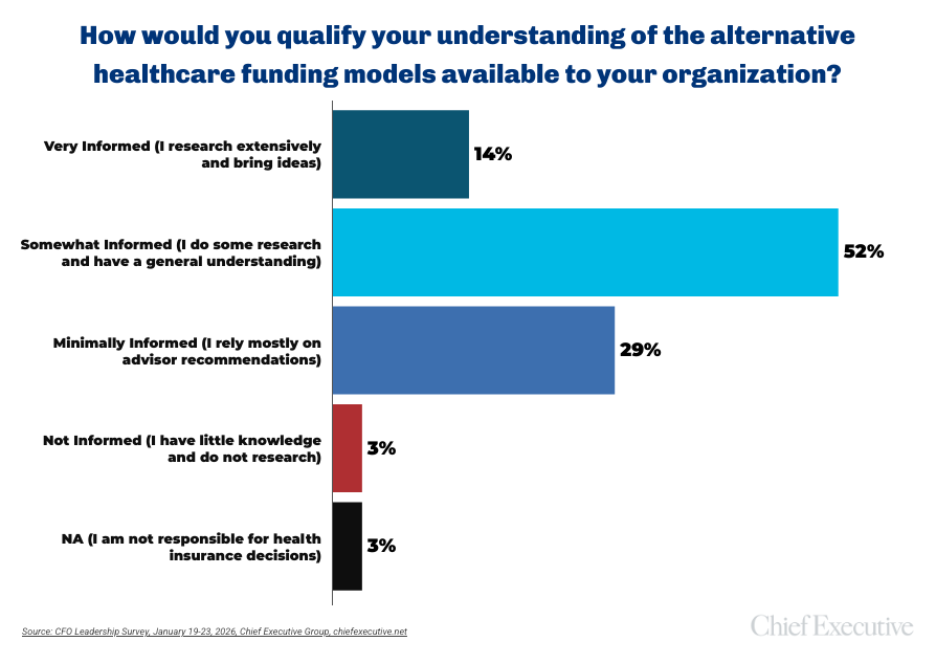

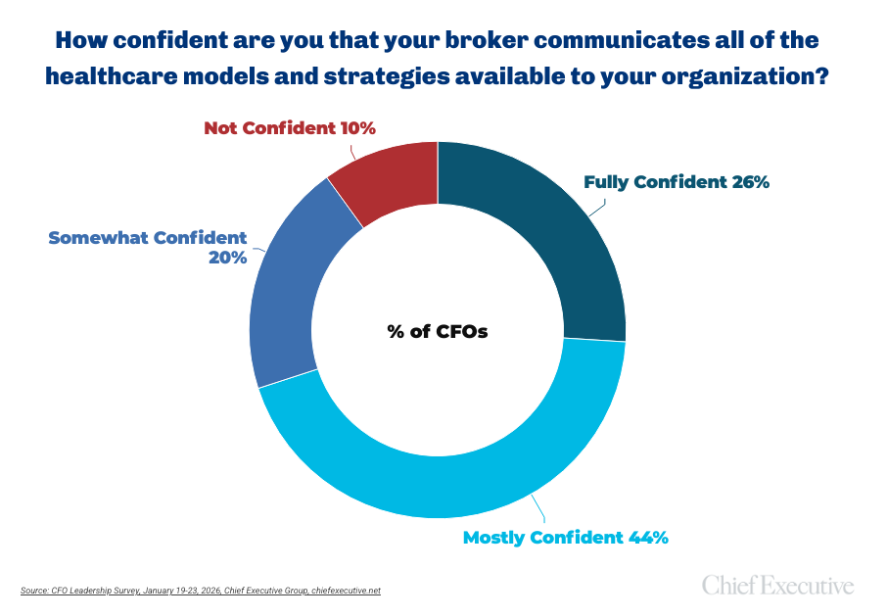

Only 14% of CFOs feel “well-informed” about alternatives to traditional healthcare models. At the same time, 95% say they trust their brokers and advisors to provide more complete and unbiased information than other sources, and 70% say they are confident that their broker will tell them all the healthcare models and strategies available to their organization.

Some executives describe the issue as limited influence rather than indifference. As one CFO explains, “There is little transparency or flexibility, and cost increases by carriers can sometimes be surprising.” “In some cases, you may have to respond only to carrier requests to avoid changing carriers and disrupting your employees.”

Michael A. Schroeder, founder and president of Roundstone Insurance, said employers often wait too long to evaluate plans, narrowing their options. “Employers need to get out of the mindset that they’re looking at a 12-month cycle with two months left in the calendar or fiscal year,” Schroeder says. “That approach would put us in a bad situation where we would find out there was a 20 percent increase in November.”

Rather, he says, leadership teams that start evaluating options early in the year may be more flexible when renewal season arrives.

Pay more, receive the same

Adding to the pressure is the fact that rising premiums have not consistently translated into better benefits.

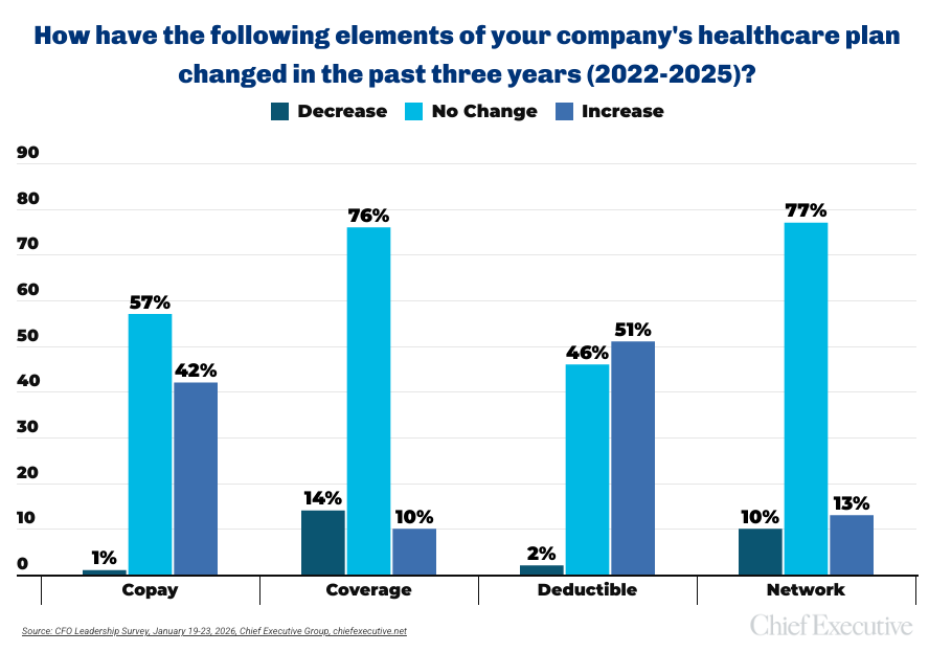

Some of the CHROs we surveyed include:

- 76% said their coverage would remain the same despite the higher premiums.

- 14% said the coverage had worsened.

- 77% report no improvement in their provider network.

- 57% said their out-of-pocket costs remained the same, and 42% said they had increased.

- 51% report higher deductibles.

This pattern shows a discontinuity. Although organizations are paying more, most report no measurable improvements in coverage breadth or benefit design. At the same time, increases in employee contributions and out-of-pocket costs can reduce the real value of wage increases.

“If you want your employees to pay more through higher copays and deductibles, give them the tools to become better and smarter shoppers,” Schroeder says. “It's their money. Let's let them pursue quality, deliver better results, and be more cost-effective.”

Predictability premium

Even with increased costs, predictability appears to be more important than outright reduction.

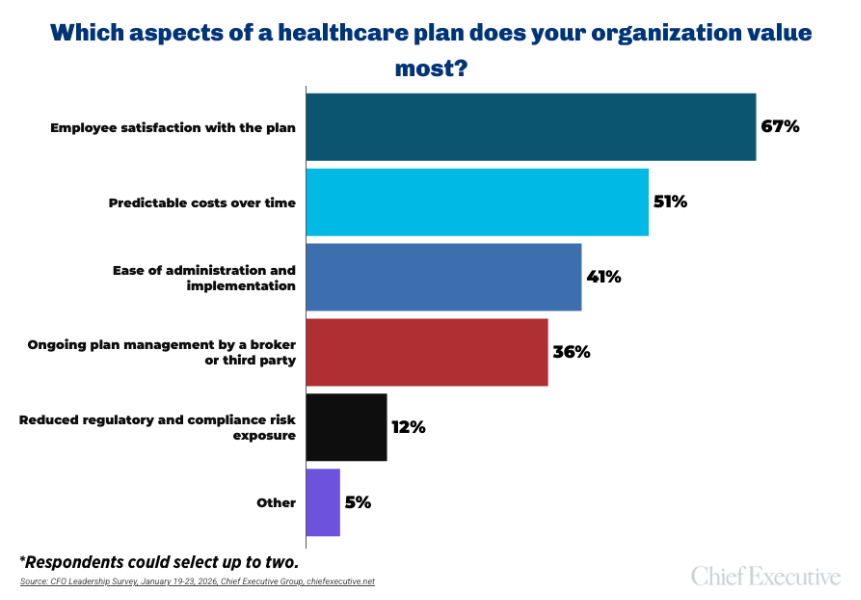

When asked which aspect of healthcare planning their organizations value most, 67% of CHROs cited employee satisfaction. “Predictable costs” came in second place, selected by 51%. Ease of administration follows at 41%, with 36% pointing to ongoing plan management by a broker or third party. Only 12% said their regulatory and compliance risks have been reduced.

The emphasis on predictability suggests that volatility itself, not just absolute costs, is a central concern. For many employers, budgeting, workforce planning, and total compensation strategies are complicated by the inability to reliably predict annual increases.

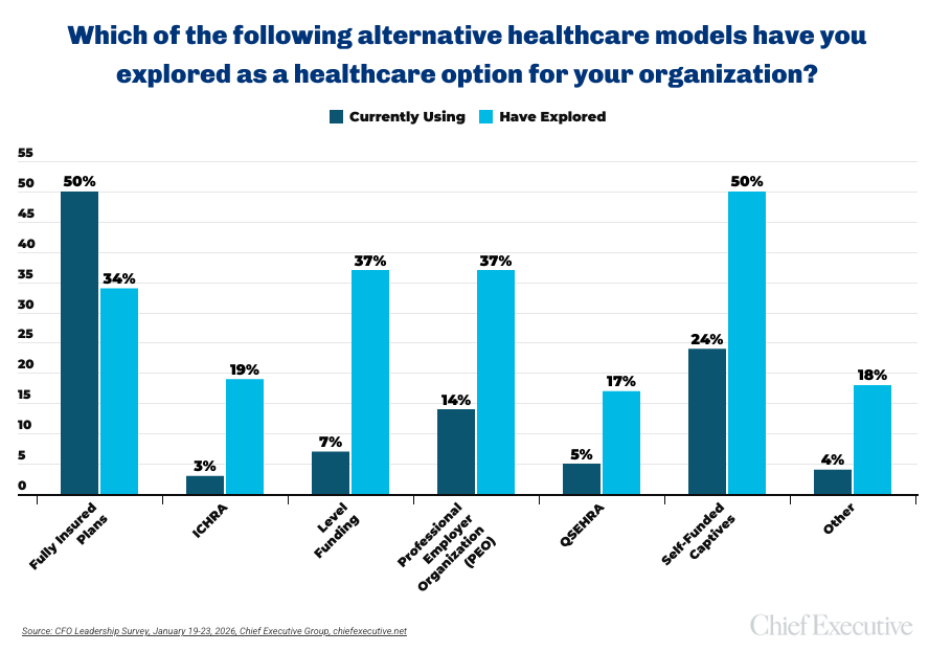

Approximately half of CFOs surveyed said they are considering a self-funded captive model as an alternative solution over any other structure, including ICHRA or QSEHRA arrangements, but it remains unclear whether that consideration will lead to adoption.

“Five years ago, many employers thought they had no choice and were stuck in an environment where they didn't know why costs were going up. Things are much better,” Schroeder said. “We have a long road to improvement, but we are making good progress.”