As a follow-up to last year's study of the first 100 S&P 500 proxy filers of 2025, Pearl Meyer examined executive compensation disclosures for 37 S&P 500 companies with fiscal years ending between August and November 2025 and that filed shareholder proxies by February 6, 2026. Our focus was on examining trends related to topics of current interest among compensation committees.

Pearl Meyer's early 2026 review identified three notable findings. The first two of these continue the trends identified in the 2025 review, and the third is new for 2026.

- Increased CEO security and aircraft benefits

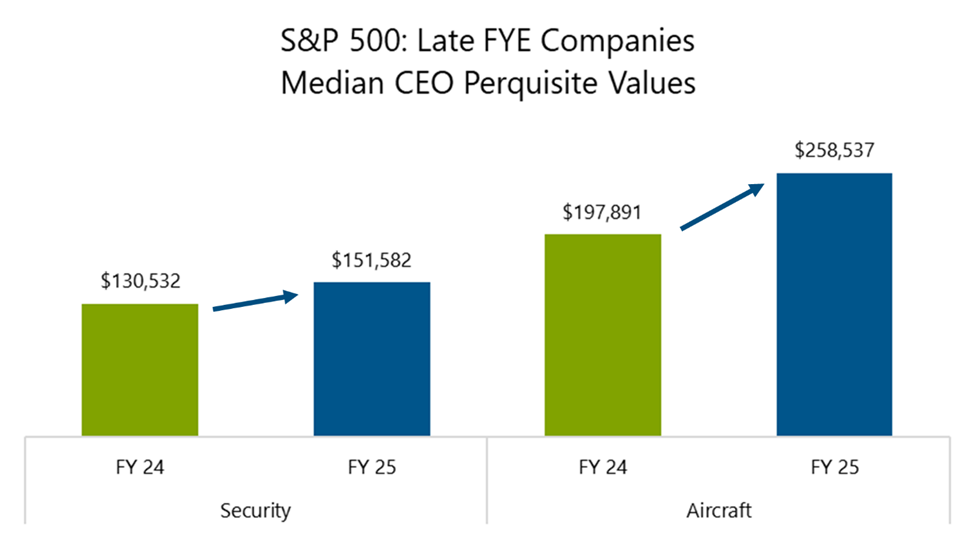

In addition to the increased prevalence of security and travel-related perks, we also found that the median security and aviation perks for the same incumbent CEOs also increased by 16% and 31%, respectively. - DEI and ESG related adjustments

We found that 22% of companies have removed the word “diversity” from their proxy statements. Additionally, approximately one-third of companies with goals related to environmental, social, and governance (ESG) and diversity, equity, and inclusion (DEI) have removed or “restated” those programs while maintaining the overall spirit of their efforts. - The impact of tariffs on executive compensation will be minimal.

Although the United States and many other countries imposed a number of tariffs after fiscal year 2025 incentive targets were set, we found that only 6% of companies adjusted their targets or outcomes to offset the impact of tariffs on executive compensation.

Overall, companies appear to be responding to the changing external environment by placing greater emphasis on risk monitoring, evolving disclosure practices, and prudent exercise of discretion.

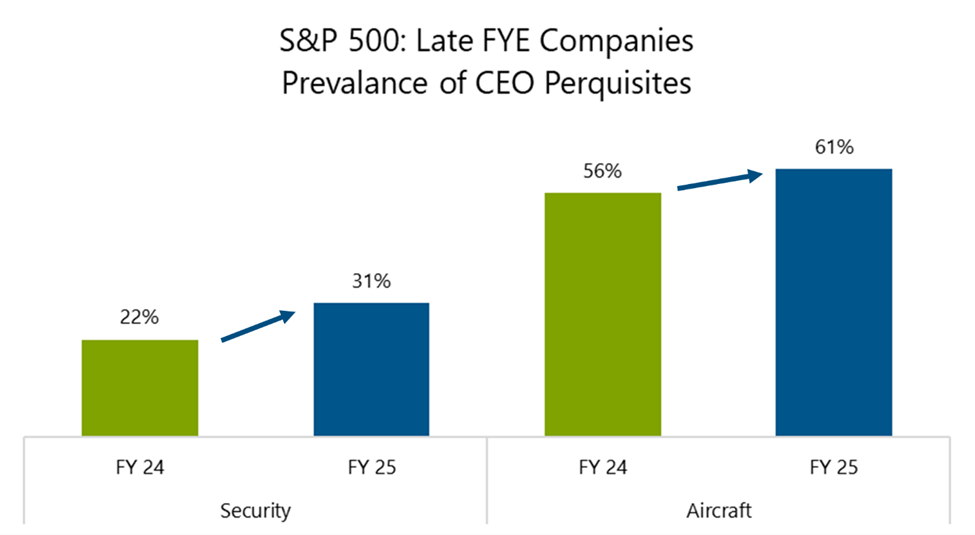

CEO security and aircraft perks continue to increase

Following the assassination of UnitedHealth's CEO in late 2024, the public company's board of directors took steps to assess the security risks of its executives and take security measures as necessary. Regarding security and aircraft perks, the chart below shows that both the prevalence and value of these perks are increasing for companies with fiscal years in late 2025.

As shown above, 31 percent of companies mentioned security prerequisites, up from 22 percent last year, and 61 percent mentioned aircraft prerequisites, up from 56 percent last year. Furthermore, their median values increased by 16 and 30 percent, respectively (see below).

As security and aviation benefits have increased in popularity and value, we have seen a shift in disclosures that describe these benefits as part of an integrated protection plan rather than convenience benefits. Specifically, many companies base their decision to offer security and aviation benefits on third-party security assessments and identified risk factors. In some cases, companies go further and say they require certain protections.

Taken together, these findings suggest that as investment levels rise, security is increasingly framed as a board-level governance and risk issue rather than a discretionary benefit. This may represent a rapidly evolving story, given that Pearl Meyer's December 2025 Executive Security Quick Poll of more than 250 companies found that many organizations are, in fact, still lagging behind in formalizing their approaches.

For example, the poll revealed that 66% of respondents spend less than $10,000 annually on CEO security, and this concentration appears to confirm that many companies treat security as an occasional cost rather than a comprehensive annual program. The survey also found that 53% of respondents include private air travel in their CEO security program (compared to 61% in the early 2026 survey). It will be interesting to see if its prevalence increases as more companies file proxies in 2026. We expect penetration rates to vary by company size and industry, with larger and consumer-facing companies likely to disclose higher penetration rates and the associated value of security-related benefits.

ESG and DEI rebranding remains popular

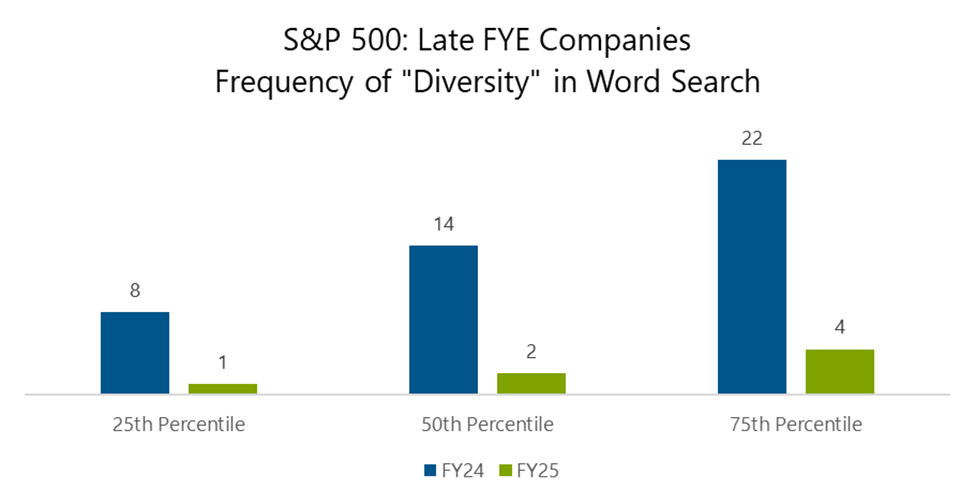

Companies continue to move away from using DEI-related measures in executive incentives. As shown in the graph below, the usage of the word “diversity” in proxy statements has decreased noticeably.

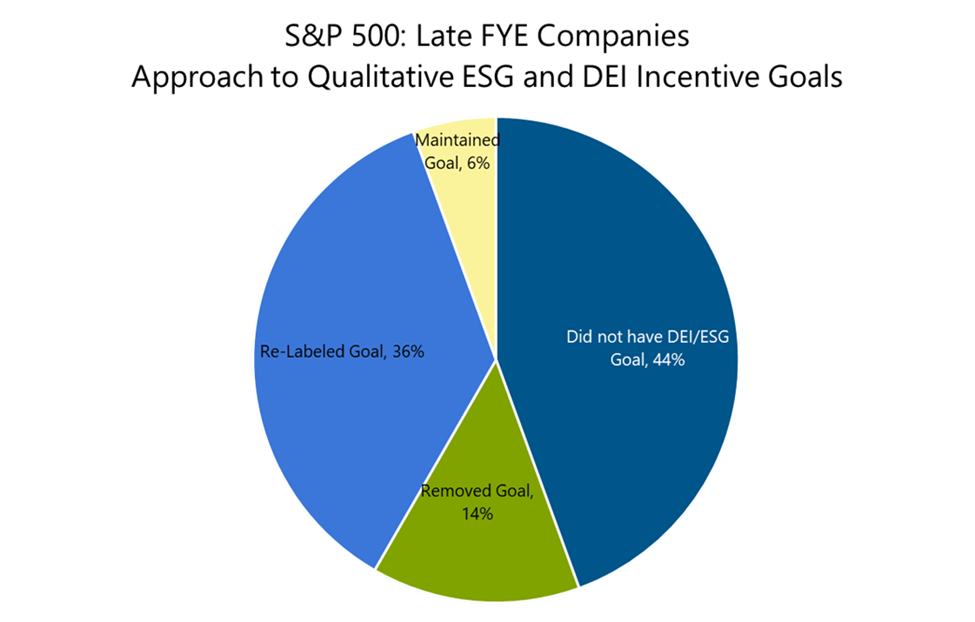

Additionally, we are seeing a shift in the use of qualitative ESG and DEI goals in incentive plans. 14% of companies removed their DEI or ESG goals, and 36% of companies “restated” their DEI or ESG goals. Only 6% of companies in our sample maintain diversity-related goals in their incentive programs. This compares to last year's study, which found that 35% of the first 100 S&P 500 proxy applicants had diversity as a factor in their 2024 incentive programs.

An example of goal “relabeling” is when an S&P 500 company changed the wording of a goal in its strategic incentive plan from “diversity and inclusion” to “talent strategy.” Additionally, another company shifted its metrics from “diversity, equity, and inclusion” to “environment and human capital” in its CEO incentive compensation disclosure.

In general, these changes suggest that while fundamental priorities around human capital and sustainability may remain, companies are increasingly reshaping how these goals are articulated and incorporated into executive compensation.

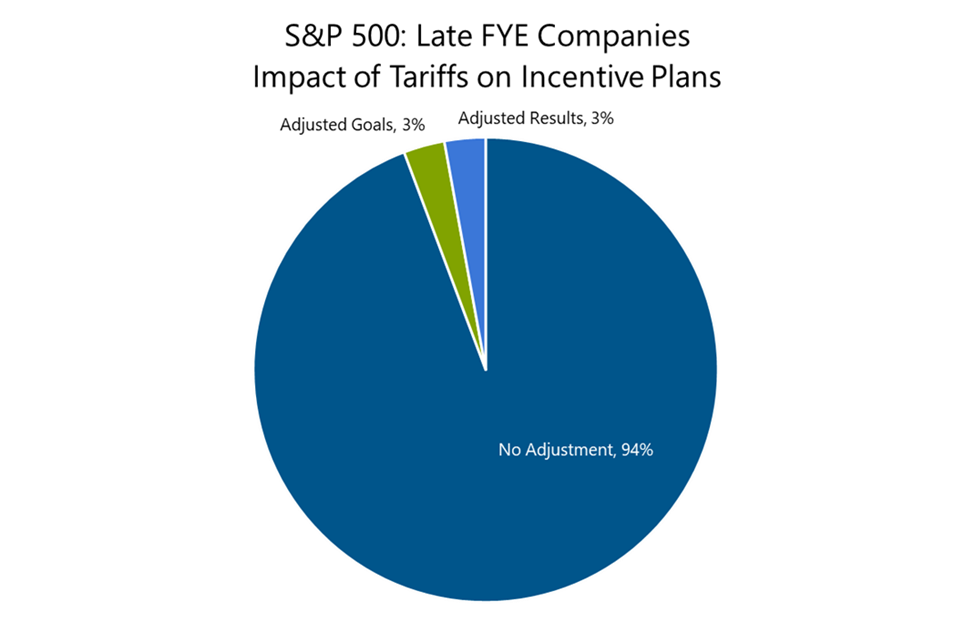

Tariffs had minimal impact on executives' annual incentive plans

We found that among S&P 500 companies in the second half of fiscal year 2025, 94% did not adjust for the impact of tariffs on executive annual incentives in fiscal year 2025. In the limited cases in which firms adjusted for the impact of tariffs, there was a mix of target adjustments and actual outcome adjustments. Some companies may have made adjustments to a broader workforce rather than executive officers, thus avoiding disclosure. Proxy disclosures regarding active exercise of discretion to adjust management incentives may lead to scrutiny from investors and proxy advisors, but adjustments below the management level are not disclosed and therefore not subject to scrutiny.

The recent Supreme Court ruling that President Trump does not have the authority to impose tariffs and the resulting obligation to repay the duties paid has made the issue even more difficult to navigate. We expect relatively little exercise of discretion outside of significantly affected companies. However, we expect more companies to incorporate tariffs as a potential adjustment factor when setting targets for 2026, something they did not have the opportunity to do in 2025.

These statements only give an initial look

Of the 37 proxy statements reviewed, companies appear to be taking a cautious approach to discretion, assessing how personal safety concerns, policy changes, and geopolitical risks may impact future incentive targets. As more companies file proxies throughout 2026, these early signals could help compensation committees anticipate how evolving risks will impact executive compensation design and disclosure.