")

4kodiak/iStock Unreleased via Getty Images

Investment Thesis

I have made some previous bullish claims about Amazon (Nasdaq:AMZN) has been growing at a healthy clip since late March, even as its stock price has languished slightly compared to the broader market. My optimism is bolstered by Amazon's solid performance. Leadership in cloud infrastructure, one of the hottest industries right now. AWS's strong growth momentum and cost controls have enabled the company to aggressively grow free cash flow. [FCF] This is the metric that matters most to me as a long-term investor. Based on my valuation analysis, the stock is undervalued by about 35%. Overall, I reiterate my “Strong Buy” rating on AMZN.

Recent developments

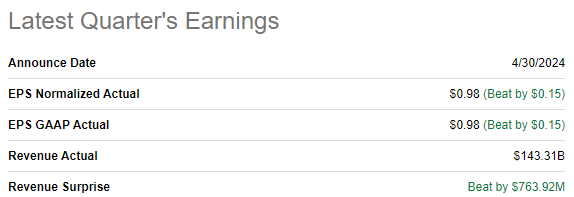

AMZN reported its latest quarterly results on April 30, beating revenue and EPS expectations. Revenue grew 12.5% year over year, and adjusted EPS grew from $0.31 to $0.98. The e-commerce business was strong in North America and Europe. In the U.S. and internationally, the cloud business also showed strong momentum with AWS revenue up 17%. Digital advertising also showed strong momentum with impressive growth of 24% year over year.

Find Alpha

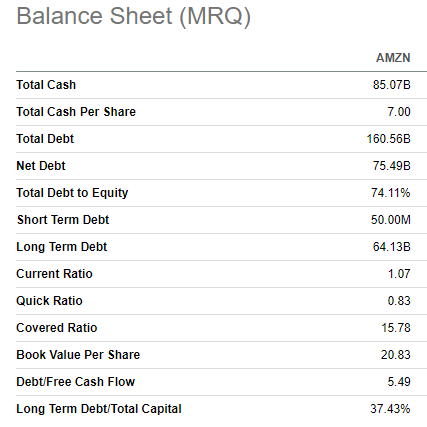

Strong sales growth across all business lines helped Amazon unleash its operating leverage. Operating margins expanded from 3.8% to 10.7% year-over-year, a significant improvement. The strong quarter enabled Amazon to generate $5.6 billion in free cash flow, which certainly contributed to an already strong financial position. AMZN ended Q1 2024 with a massive $85 billion in cash and total debt, well below the company's market cap of $1.9 trillion. Amazon's strong balance sheet is a competitive advantage for the company as it provides it with enormous opportunities to invest in growth and innovation.

Find Alpha

AWS remains the undisputed leader in the cloud infrastructure business with a 31% global market share. The gap with Microsoft (MSFT) is large, but AMZN's main rival has been working aggressively to close the gap in recent quarters. To protect its industry dominance, AMZN has been investing aggressively in cloud and AI-related ventures. The company plans to invest $150 billion in AI data centers over the next 15 years, which shows management's strong commitment to maintaining AMZN's leadership in the cloud business.

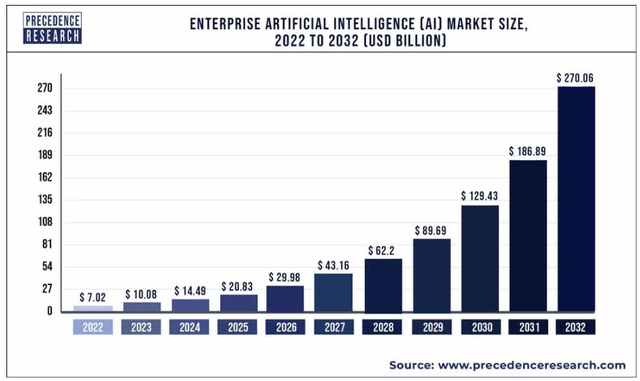

Additionally, AWS is expanding its AI capabilities to power enterprise business applications. Recent news has revealed that Amazon's Bedrock platform will be available for SAP's infrastructure services, accelerating enterprise adoption of AI. Given Amazon's dominance in the cloud and the fact that SAP applications are used by 9 out of 10 Fortune 500 companies, this partnership is likely to be very strong. Apart from the potential synergies, it is important to highlight that the enterprise AI solutions industry is growing rapidly. Precedence Research predicts that the industry will grow at a CAGR of 44% over the next decade.

Previous research

AWS is not only partnering with big companies like SAP and investing billions in data centers, but also scouting for promising superstars among AI startups. And since Amazon offers AWS credits to these startups, they often don't even need to support them with cash. That said, AWS' strategic approach to maintaining its strength in the AI space seems holistic, as it invests billions in in-house R&D and infrastructure, seeks strategic partnerships with other large companies to expand its reach, and scouts for promising stars among early-stage startups. This approach seems reasonable in my opinion.

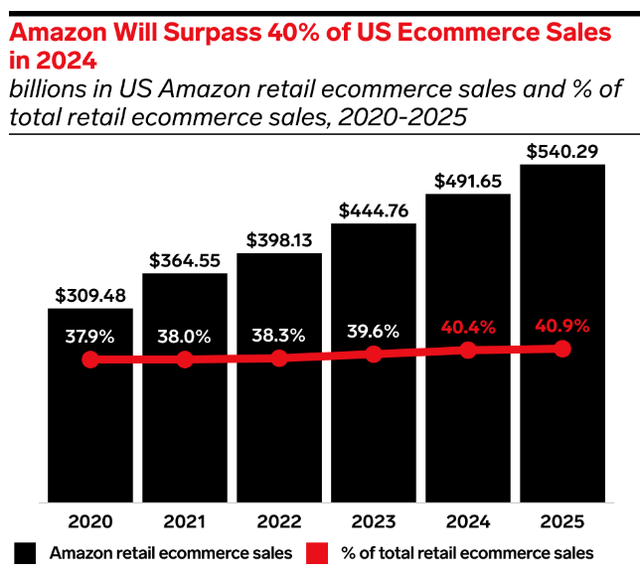

E-commerce, the company's largest business by revenue by far, continues to hold an unmatched position in the industry: Amazon's U.S. e-commerce market share is expected to continue growing through 2024-2025, exceeding 40%, according to EMarketer.

E-Marketer

Amazon Prime's subscription-based business continues to develop, and a partnership with Grubhub was recently announced. With this partnership, Amazon continues to provide more value to Prime members, as members will receive additional benefits from Grubhub as a result of this collaboration. The company is also working to improve the e-commerce experience for Prime members, and the first quarter saw the fastest delivery speeds in the company's history. According to the first quarter earnings report, about 60% of Prime member orders arrived the same day or the next day across the top 60 metropolitan areas in the United States. With new collaborations and efforts to improve the experience of paid members, this business could also contribute to the company's overall success.

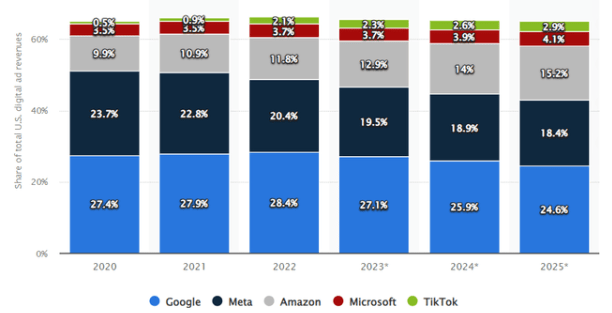

Its strength in expanding its e-commerce business also helps it build other promising businesses. For example, Amazon's vast e-commerce customer base has allowed it to build a robust digital advertising business, which is thriving with 24% revenue growth in Q1 2024. In the bar chart below, we can see that Amazon's market share growth in the digital advertising industry is showing strong momentum, with the company expected to capture a commanding 15% market share by 2025.

Statista.com

To summarize this piece, Amazon continues to show strength across all of its businesses. AWS will likely remain Amazon's primary growth driver for the foreseeable future, and we like the holistic approach management is taking to maintain its market leadership and maximize the potential of AI. Amazon's unparalleled position in e-commerce makes it an attractive partner for other services, and new collaborations will add value to Prime members and help Amazon maintain momentum in its subscription-based business.

Rating Update

The company's shares have risen 45% over the past 12 months, outperforming the overall U.S. market. Year-to-date performance has also been strong, with shares up 21%, outperforming the S&P 500. Valuation ratios are often lower than historical averages, meaning the stock is likely undervalued.

Find Alpha

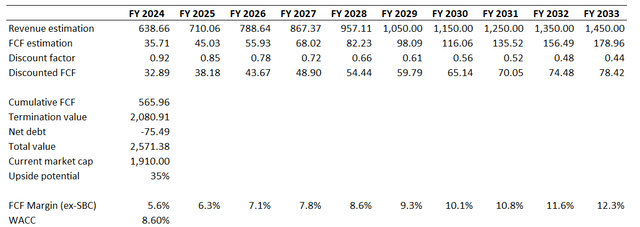

As always, I rely on discounted cash flows. [DCF] This is the most commonly used approach when drawing conclusions about a company's valuation. I use a WACC of 8.6% for AMZN as recommended by valueinvesting.io. Consensus earnings forecasts predict a 9.54% earnings CAGR over the next 10 years, which I believe is conservative enough for my DCF model. This confidence is bolstered by Amazon's historical revenue growth levels and dominance in cloud and e-commerce. Additionally, Amazon is investing heavily in research and development, increasing its potential to grow new, superior businesses.

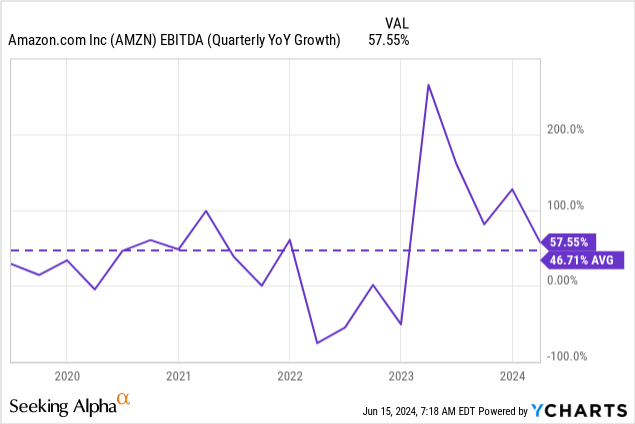

EBITDA has also shown aggressive growth over the past five years, which gives me great optimism about the company's ability to aggressively expand FCF margins.As such, I expect the company to be able to expand its 5.6% TTM ex-SBC FCF margin by at least 50 basis points annually.

Author's calculations

According to my DCF simulation, AMZN is fairly capitalized at approximately $2.6 trillion, which is 35% higher than its current market cap. That said, the upside potential is attractive and I can confidently conclude that AMZN stock is a bargain at the current price.

Risk Update

My valuation analysis is based on expectations of long-term revenue growth and FCF margin expansion. Given Amazon's dominance in cloud infrastructure and e-commerce, there is ample reason to believe in Amazon's growth potential. Apart from its strong strategic positioning, my optimism is also firmly supported by Amazon's past success. However, we all need to remember that past success is no guarantee of future growth. There are a number of significant risks that could undermine Amazon's growth potential.

Amazon's position in e-commerce is unmatched, but its competitive risks in the cloud business are much higher. Amazon competes with Microsoft and Google in the cloud, which has dominated the PC software market for the past 30 years. Google's position in digital advertising is unmatched, making the company an FCF machine that can invest in AI R&D and acquisitions. Given Amazon's size, antitrust authorities may also impose regulatory obstacles on the company's growth prospects.

As Amazon's international e-commerce business expands, it is likely to face growing currency risks, too, as a strong U.S. dollar is likely to be a constraint on the profitability of its international operations.

Conclusion

In conclusion, AMZN remains a Strong Buy. Recent developments have increased my confidence in the company's growth prospects as the company is showing strength across all business lines and its significant investments in growth are likely to pay off in the long term. AMZN's valuation remains very attractive with upside potential of 35%.