Published as part of the ECB Economic Bulletin, issue 8/2023.

The policy rate hike cycle that began in mid-2022 has prompted banks to increase the interest rates they offer on deposits. The ECB has so far raised the three main interest rates by 450 basis points during the tightening cycle. Compared to levels at the end of May 2022, just before the intention to raise interest rates was announced at a press conference in June, the newly agreed interest rate on fixed deposits has increased by 372 basis points, and the interest rate on overnight deposits has increased by 50 basis points. . .

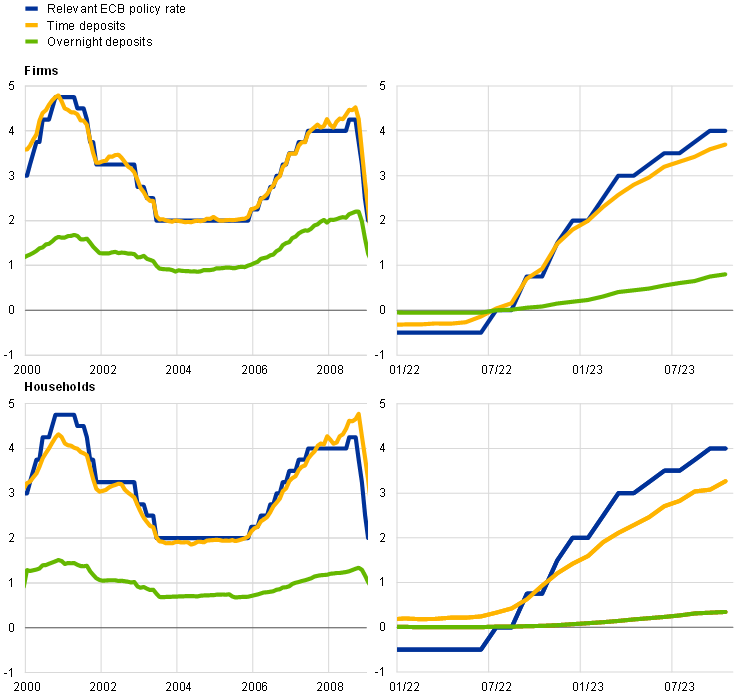

Nevertheless, deposit rates, particularly for households, primarily overnight deposits, remain slightly below historical levels when compared to policy rates. When interest rates are positive, term deposit rewards tend to roughly follow the policy rate.[1] In October 2023, euro area businesses and households were offered, on average, annual interest rates of 3.70% and 3.27%, respectively, on newly agreed term deposits with two-year maturities. This means the spread over the policy rate is -30 basis points and -73 basis points, respectively. Spreads on corporate term deposits were within historical ranges in October, while spreads on household term deposits widened slightly but were not unprecedented, at the height of the 2000-2001 monetary tightening cycle. It was almost similar to what was observed in early 2001. In contrast to term deposits, overnight deposit rewards are typically significantly above the policy rate, reflecting the payment, liquidity, and convenience services offered by site deposits, where interest rates are well above zero. (Chart A, panel a).[2] Associated rewards also move slowly. This means that the size of the resulting spread over the policy rate tends to widen during tightening cycles. This widening is consistent with the idea that high switching costs give banks market power, especially in the site deposit market.[3] In October 2023, the inverse spread on these deposits widened significantly compared to the 2007-2008 period, and interest rates stabilized at the peak of the rising cycle, but less so compared to the plateau reached in the 2000 cycle. There wasn't. However, it should be considered that deposit fees in 2007-2008 may have been partially supported by banks' liquidity needs as the global financial crisis began to unfold. In contrast, current economic cycle trends also appear to be partly influenced by banks' lower demand for funds, against a backdrop of weak lending and reduced competition in some segments of the deposit market. .[4]

Cumulative changes in deposit interest rates are relatively weak. This is partly because deposit rates were above policy rates during the period of negative interest rates that preceded this cycle, but also because the spillover to household overnight deposit rates was actually weak. . The rate of increase in deposit rates relative to the rate of increase in policy rates is a widely used measure to compare the strength of interest rate pass-through to deposit rates across a tightening cycle. This ratio is commonly referred to as the deposit beta. However, this measure is sensitive to the starting point, particularly if the spread between the deposit rate and the policy rate at that point differs from historical norms. This was the case at the start of the current tightening cycle, as the spread between deposit rates and the policy rate turned negative by mid-2022 (Chart A, panel a, right graph). This reversal in deposit spreads reflects the fact that banks have been reluctant to pass on negative interest rates to retail depositors, citing legal barriers, litigation risks, or concerns about deposit withdrawals.[5] The end of the era of negative and ultra-low interest rates has allowed the spread between policy and deposit rates to return to historical patterns, ushering in a period in which policy rate hikes are matched only by small increases in deposit rates. . Therefore, when using deposit beta to compare the strength of deposit rate pass-through with past episodes, it is important to exclude periods when policy rates are low. For example, it would be possible to exclude periods when the policy rate was below 2%, the level at the start of the previous cycle. When this happens, the deposit beta of all overnight deposits and term deposits held by households increases. The fact that businesses and households now make a higher proportion of overnight deposits than in the past is another factor that weights the aggregate deposit beta, i.e. the rise in deposit rates across different deposit types based on balances. Yes (Chart B, Panel B). . If we use deposit shares from the 2005-2007 tightening cycle (instead of current equities) to blend overnight and term deposit rewards, the resulting deposit beta, although still slightly lower, is (graph) A, panel b). This is mainly because the transmission of policy rate hikes to overnight household deposits is really weak.

Chart A

Passing on interest rates in the euro area

a) Interest rate level

(Annual rate)

b) Beta deposit

(percentage)

Source: ECB.

Note: For term deposits, the interest rate is for new contracts with a maturity of less than two years. Deposit beta is defined as the ratio of the increase in deposit rates to the increase in the policy rate. His latest observations are from October 2023.

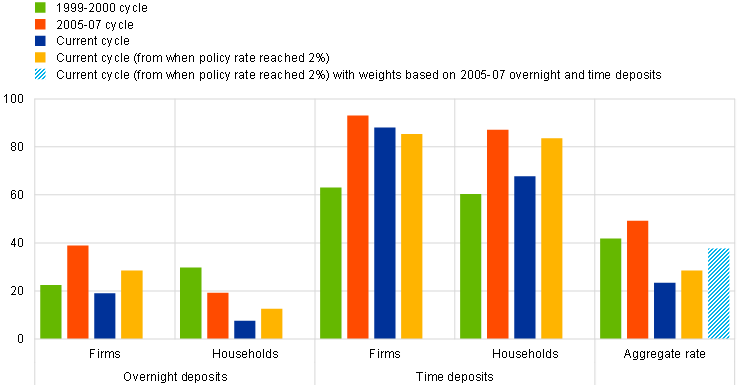

Increasing rewards for fixed deposits and bonds after a long period of low or negative interest rates has encouraged a shift away from overnight deposits and other low-reward deposits to these products. In an era of low interest rates, the opportunity cost of holding overnight deposits was so low that households and businesses accumulated almost all of their new capital balances in overnight deposits (Exhibit B, Panel a). The current tightening of monetary policy, and its spillover to deposit rates and yields on other financial assets, has increased the opportunity cost of holding overnight deposits to levels similar to those seen in past rate hike cycles. ing. As a result, companies and households have been forced to transfer a significant portion of their unusually large overnight deposits into time deposits and bonds. The stock has shrunk compared to mid-2022, but is still high by historical standards. This is more pronounced for households than for firms (Exhibit B, panel b).[6] This could explain the slower shift in deposits by businesses observed over the past two quarters.

Chart B

Portfolio rebalancing

a) Financial investments by businesses and households

(Left scale: quarterly flows, billions of euros; right scale: percentage points)

b) Overnight deposit

(Percentage of total deposit holdings)

Source: ECB.

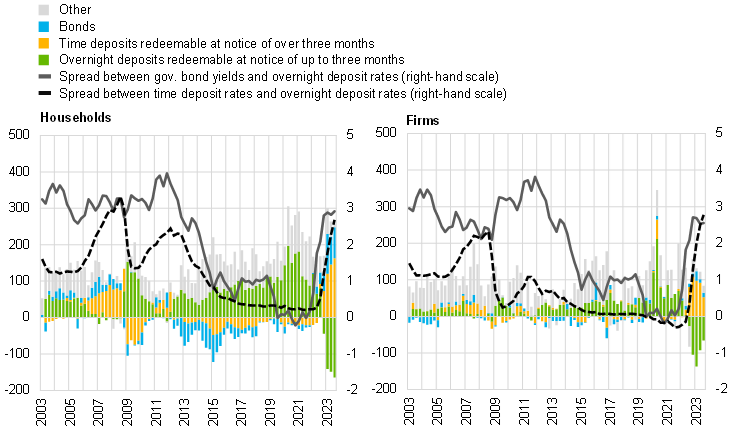

In general, changes in monetary policy not only affect portfolio decisions by households and businesses, but also affect money creation in a variety of ways. First, when a bank provides credit, through credit creation, an increase in the borrower's deposit balance is immediately reflected, and the borrower's deposit balance becomes available for payments and other transactions.[7] Second, in a similar manner, when a central bank acquires assets from a euro area resident other than a bank, or when a non-resident acquires goods, services or financial assets from a euro area resident other than a bank. Also, the money balance in a broad sense increases.[8] Finally, central bank credit to banks can also lead to money creation to the extent that it replaces bond financing, thereby freeing up funds that depositors can hold in their accounts.

The current tightening of monetary policy has weakened widespread money creation, pushing it into negative territory at historic lows. Since the current tightening cycle began, rising interest rates have significantly reduced both loan demand and loan supply. This significantly reduced the amount of credit, which is a typical source of money creation. Furthermore, the contraction of the Eurosystem's balance sheet intensifies the decline in credit supply, which in turn has a direct impact on M3 through two channels. (i) TLTRO Repayments. This encourages banks to issue long-term bonds, resulting in a decrease in the money balance. Depositors acquire these bonds. (ii) gradually redeem the asset purchase program portfolio and remove funds from circulation;[9] As a result, the contribution of lending to businesses and households to annual M3 has fallen from 4 percentage points in mid-2022 to almost zero in October 2023, while bank bond issuance is now around 1.5 percentage points from annual M3 stock. It's sucking away percentage points. The direct contribution from Eurosystem purchases turned negative, from nearly 6 percentage points at the beginning of 2022 to -1 percentage point in October 2023. However, although there has been a decline in government bond purchases by households, this has been almost offset by government bond purchases by foreign investors. Currently, we are placing some weight on financial trends. The return to current and capital account surpluses, which also reflects weakening domestic demand for foreign goods, will further support net foreign capital inflows from the second half of 2022 onwards (Exhibit C, Panel a).

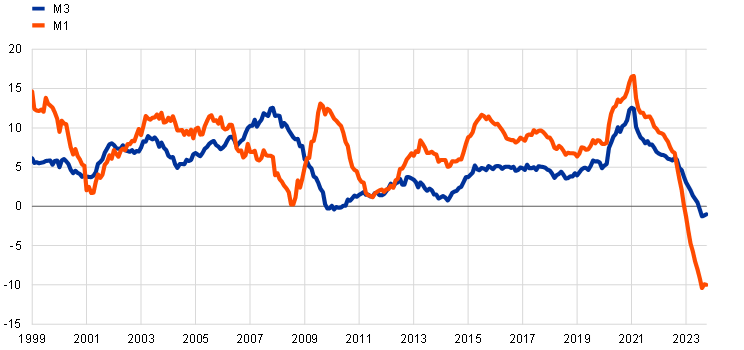

Chart C

currency aggregation

a) Source of money creation

(Change in annual percentage, contribution to change in annual percentage)

b) Currency aggregation

(Annual rate of change)

Source: ECB.

Note: Latest observations are from October 2023.

The movement of deposits and the contraction of widespread money led to an unprecedented magnitude of negative growth in the narrow monetary aggregate M1. Since overnight deposits are a major component of M1, the shift away from them has resulted in an unprecedented contraction in this aggregate (about 10% since the summer, Exhibit C, Panel b). Given that M1 growth has historically been a good predictor of real GDP growth, there are concerns about a further slowdown in economic activity.[10] Since M1 is a relevant indicator of the degree of liquidity in the economy, this relationship partly operates through consumption, savings, and investment decisions. However, in the current situation, the continued shift away from overnight deposits and the strong growth in M1 since 2015 (which was mainly related to a combination of net asset purchases and low interest rates) are showing signs of normality. It may be ambiguous. In other words, a decrease in M1 due to a portfolio shift away from overnight deposits should, in principle, have a more muted impact on agents' spending capacity. Therefore, the negative impact on GDP should be less than a typical decline in M1, especially given that overnight deposit balances remain relatively high by historical standards. However, this does not mean that M1 should be completely excluded, especially in cases of financial market tensions and increased liquidity demand.