Members of the boards of U.S. public companies feel the current business environment is better than it was three months ago, even though most of the issues weighing on business, from geopolitics and trade policy to macroeconomic uncertainty and market volatility, remain largely unresolved.

However, their increased confidence does not suggest a clear upward trend in the second half of 2026.

in corporate directorIn Diligent Institute's second-quarter Director Confidence Index, conducted June 3-8, directors rated current business conditions at 5.9 out of 10, up from 5.6 in the first quarter. This 6% improvement returns the Board Current Rating to the range that has defined board sentiment since the index's inception six years ago. I'm not pessimistic, but I'm not particularly enthusiastic either.

Directors' outlook for the year ahead is similarly subdued. Directors expect the business situation to remain essentially unchanged one year from now, giving it a score of 5.9 out of 10. While this is flat compared to the current environment, it is still an 8% increase from Q1 expectations and a positive change from 2025, when both the current rating and forward outlook fell into the low-to-mid 4 range.

“The second-quarter survey results suggest that confidence is stabilizing rather than spiking,” said Kira Ciccarelli, senior research manager at the Diligent Institute. “This makes sense in the context of the GC Risk Index, where overall risk remains high. As long as risk levels remain high, confidence is likely to continue to be measured rather than fully recover to pre-2025 levels.”

opinions are divided

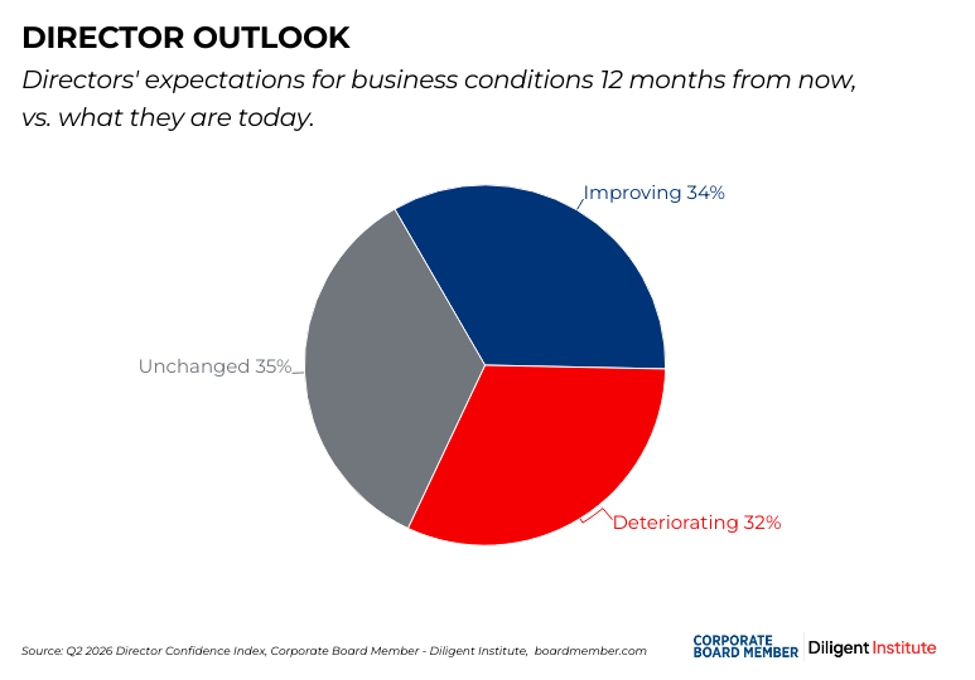

The survey results also revealed that opinions are divided across U.S. boardrooms.

Of the 104 directors surveyed, 34% expect business conditions to improve over the next year, while 35% expect little to change and 32% expect conditions to worsen.

This division is consistent with the history of the index. The director's emotions rarely swing to extremes. Even in good times, their current and forecast ratings tend to hover around the middle of a 10-point scale. This is a reminder that their role is to look around the corner, test assumptions and consider downside risks.

Uncertainty was a recurring theme in directors' outlooks this quarter, including policy and regulatory changes, geopolitics, inflation and interest rates.

Among those predicting a worsening economy, many commented on inflation, interest rates, tariffs, and global conflicts. Optimistic directors cited some of the same factors, but with different expectations that inflationary pressures, interest rate uncertainty and policy disruption could ease.

“Current inflation rates and poor leadership from the federal executive are causing unprecedented instability and uncertainty, causing substantial damage to U.S. relationships around the world,” one board member said, explaining the cause of the current pessimistic outlook. However, they said, “We expect both to improve after November.”

Most optimistic comments were similarly rated as less than enthusiastic. Directors who expect improvement will describe the outlook in terms of stabilization rather than acceleration, such as improved prospects, easier interest rates, greater policy predictability, improved demand, or a return to more normal operating conditions.

Some comments pointed out market risks. “We are concerned about the AI and IPO boom. This could result in significant overvaluation leading to trust issues,” one board member wrote.

Others shared concerns about the rise in private and consumer credit, the impact of AI on businesses and the workforce, and the slowdown in the housing market. At the same time, some respondents pointed to opportunities for growth and resilient strategies to weather rough waters.

Agility may help explain some of that divergence. Small businesses are often able to pivot more quickly in response to changing circumstances. Directors of companies with less than $500 million in revenue were more optimistic than their larger peers, with only 17% expecting conditions to worsen.

By comparison, half of directors at companies with sales of $5 billion to $9.9 billion expect business conditions to worsen over the next 12 months. Among companies with revenues of $10 billion or more, 42% expect conditions to worsen.

Sectoral differences also indicate environmental heterogeneity. Directors of companies in the technology industry are among the most optimistic, with an average 12-month forecast of 6.5 and 44% expecting the situation to improve. The most cautious view is seen in the power and utilities sector, where directors expect the situation to fall from the current 5.8 to 5.2 in a year's time.

Committee representatives offer another perspective. Risk committee members are more likely to predict improvement: 47 percent say things will be better in a year's time, compared to about a third of all directors. That doesn't necessarily mean risk committee members are less concerned. One possible explanation is that they are closely tracking the same set of issues currently driving boardroom discussions: inflation, interest rates, geopolitical volatility, policy uncertainty, and business model resilience.

Taken together, the findings suggest that the business environment, while stable, has not decisively strengthened. Directors are no longer expressing the same level of concern that characterized much of 2025, but neither are they predicting a widespread acceleration.