In the fast-paced environment of financial reporting, determining current priorities and forward-looking strategies can be difficult. Insights from audit partners at leading companies can help audit committees identify challenges and understand trends in public companies, particularly in emerging areas such as artificial intelligence.

Our audit partners have a unique perspective on the U.S. business environment given their broad perspectives and involvement in a variety of industries. CAQ's biannual Audit Partner Pulse survey provides insights from audit partners on everyday topics like the health of the U.S. economy and timely issues like investments in AI and governance structures.

The Spring 2026 edition reveals consistent findings from Fall 2025. Public companies are moving with urgency to deploy AI systems, even though frameworks are still under development. Here's what this means for audit committees.

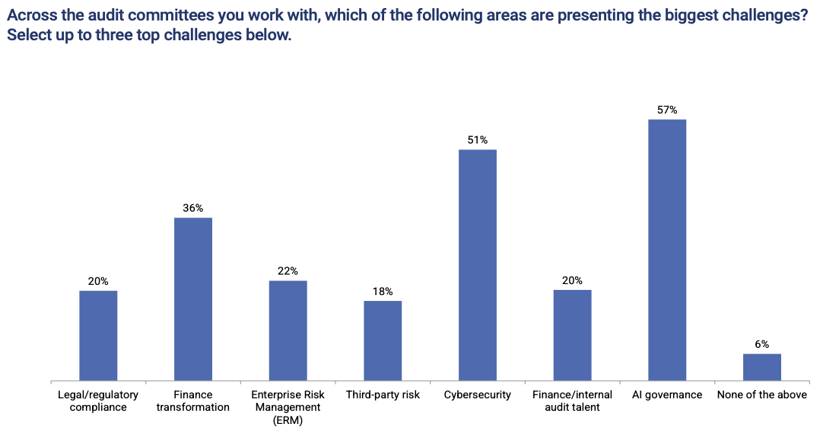

1. AI governance is the biggest challenge for audit committees today.

According to audit partners, AI governance tops the list of areas of greatest challenge for audit committees (57%), ahead of cybersecurity (51%) and financial transformation (36%). Cybersecurity has long been a priority for boards, and the 2025 Audit Committee Practices Report, jointly produced by CAQ and Deloitte's Center for Board Effectiveness, found that 50 percent of audit committees identified cybersecurity as a top priority, and 62 percent reported having primary oversight responsibilities. Fast forward to 2026, and audit partners see AI governance surpassing cybersecurity as a source of committee-level challenges, demonstrating the urgency of governance-related issues. We look forward to producing our next Audit Committee Practice Report in the coming months to compare data and auditor experience.

The same goes for governance maturity. When we asked respondents to characterize the maturity of AI governance at their largest customers, only 6% said their AI governance is advanced. This means formal frameworks, policies, and oversight structures are fully in place. A further 46% said governance was in its infancy (basically reactive), and 40% said structures had been developed but were applied incompletely or inconsistently. As boards are in the early stages of developing AI governance systems, audit committees can ask management questions about accountability, data privacy, and other safeguards to ensure the appropriate guardrails are in place.

We have outlined other AI governance considerations that audit committees should consider as companies develop their own systems and processes.

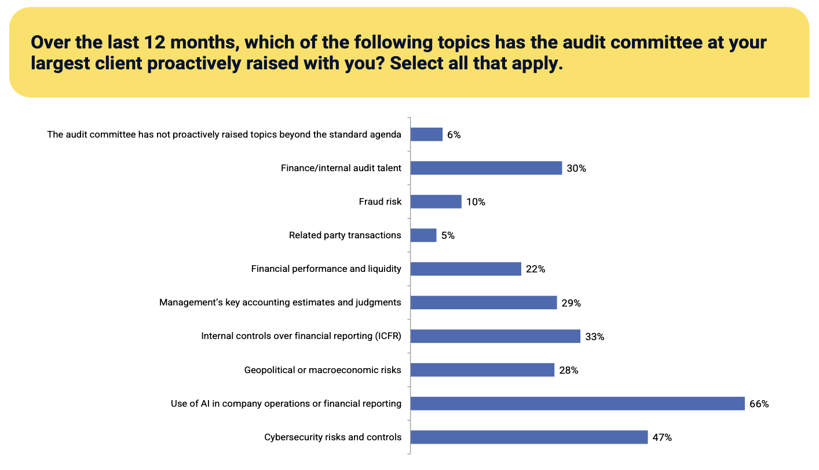

2. Audit committees are actively asking questions about the use of AI.

When asked about topics that audit committees have actively addressed in the past 12 months, two-thirds of audit partners cited the use of AI in corporate operations or financial reporting. This is the most frequently cited topic by a wide margin, ahead of cybersecurity risks and controls (47%) and internal controls over financial reporting (33%).

This highlights that the responsibilities of audit committees are expanding beyond traditional financial reporting and into emerging and complex areas of risk. As topics such as cybersecurity and sustainability become a focus for public companies, oversight by audit committees is increasingly required. A similar pattern is playing out with AI, as audit committees work to incorporate oversight of AI-related risks and opportunities into their existing agendas.

Proactively raising questions about AI with external auditing firms is an important step in ensuring that AI-powered findings are trustworthy. takeout A recent CAQ webinar helps audit committees strengthen their oversight of AI.

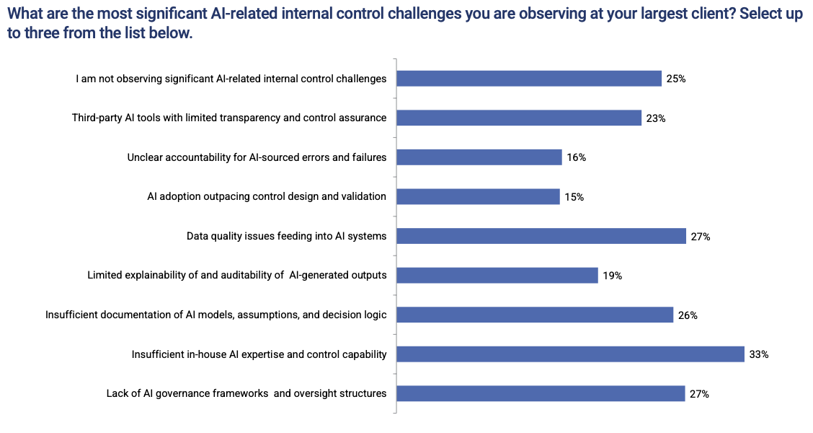

3. AI-related internal control challenges are real, not abstract.

Conversations about AI risk tend to remain at a high level, focusing on broad themes such as ethics, bias, and reputational damage. What this research uncovered is more immediate: specific operational control gaps that audit partners are currently observing in their clients' operations.

When asked to identify the most significant challenges to AI-related internal controls at their largest customers, audit partners most frequently cited the following issues:

- Insufficient in-house AI expertise and control (33%).

- Data quality issues impact AI systems (27%).

- Lack of an AI governance framework and oversight structure (27%). and

- AI models, assumptions, and decision logic are poorly documented (26%).

I recommend that audit committees use this list in their conversations with management. Ask directly whether these specific gaps exist in your organization, what controls are in place regarding the data feeding your AI systems, and whether your internal audit department has the expertise to assess them. The answer will tell you a lot about where to prioritize and monitor.

The role of the audit committee at this point is not just to monitor, but to reveal.

The Spring 2026 Audit Partner Pulse Survey reveals that AI is no longer a future state. AI is increasingly being incorporated into core judgment areas of operations, financial reporting, and audit committee oversight. Before the gap becomes an issue, the committees that are on board now will be in a stronger position as AI becomes more deeply embedded in their organizations.

Read the full Spring 2026 Audit Partner Pulse Survey.