In 2018, Tesla's board granted Elon Musk a $2.3 billion stock option package on the condition that the company's market capitalization increase 12 times over 10 years. Depending on how you look at it, this award is either the most audacious pay-for-performance design in modern corporate history or the most egregious governance failure of its time. Either way, it changed the conversation.

Since then, the boards of more than 50 large publicly traded companies have approved similar grants on a smaller scale. The conventional wisdom about these awards is wrong in important ways.

When compensation committees worry about mega-grants, they often worry about whether performance targets are aligned correctly. What if the hurdles are too high? What if you can't reach the CEO? That worry turned out to be misplaced.

An analysis of 58 performance-based CEO mega-grants implemented across the S&P 500, 400, and 600 between 2016 and 2023 found that very few failed due to poor design. Those who failed did so for completely different reasons.

Numbers every board needs to know

The median completed grant achieved 185% of grant date fair value (i.e., the number actually approved by the compensation committee), while the average was 300%. More than half of the completed grants exceeded the approved amount.

Five grants (Tesla, Oracle, RH, Charter Communications, and General Electric) were implemented more than five times. Based on the metrics that matter most to the board (what we get vs. what we approve), these grants pay out, on median, about twice the amount approved.

Companies in our sample outperformed the benchmark index in total shareholder return by a median annual percentage point of 3.2 percentage points over the performance period. The relationship between CEO dividends and shareholder alpha is approximately monotonic. Grants that realized exceptional realized values (greater than 500 percent of grant date fair value) represented companies that outperformed the index by a median annual percentage point of 37 percentage points. Subsidy equivalent to companies with zero grants poor performance Their index increased by 24.5 percentage points annually.

Performance Design did exactly what they were supposed to do: pay generously when shareholders won and pay nothing when shareholders lost. The CEO wasn't capturing market beta. They were being rewarded for truly outstanding performance.

Overall, 17% of grants were not disbursed and none had performance design failures. Six of the 36 completed grants yielded no results. All zeros were driven by something other than design. Paramount's grants to Leslie Moonves and Penn Entertainment's grants to Jay Snowden were forfeited following the CEO's firing following a reversal of the company's online sports betting strategy. Four games were canceled entirely due to circumstances that the board had not anticipated. PTC said the IAC during the Joseph Levin transition in 2025 when its grant to James Heppelmann “lost its retention value.” Paycom when Chad Ritchson became co-CEO.

None of these CEOs were able to meet their stretch targets. They left, were forced out, or were reassigned, and in each case the underlying company underperformed relative to the market.

Grants with longer durations showed substantially better performance. The five grants with a fulfillment period of more than seven years achieved a median grant date value of 953 percent. This is consistent with proxy advisor signals that extended performance and vesting periods are viewed favorably when combined with meaningful retention conditions.

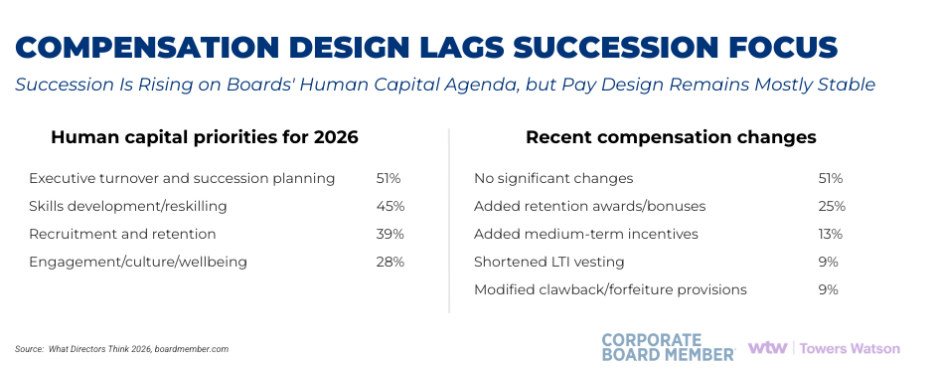

This finding is consistent with what the director himself is complaining about. In What Directors Think 2026, 51 percent of directors say executive turnover and succession planning will likely require the board's greatest attention among human capital topics this year, and 24 percent identify an unplanned departure of a CEO or key executive as their organization's biggest risk. However, 51% have not made any major changes to their compensation structures in response to shorter executive tenures, and only 18% say reviewing succession planning is a top priority for their companies heading into 2026. The gap between directors' expressed concerns and compensation design choices is exactly where this data shows.

What boards should actually worry about

If performance calibration is unlikely to be a failure mode, then what is? Three risks require more attention than usual.

CEO succession risk. Is the executive likely to remain in the seat for the entire period? Are there governance, conflicts of interest, or litigation risks that could force separation? All forfeitures in our sample follow questions that the board may have pursued more strongly on the date of authorization.

Risk of board intervention. Are there any scenarios where the board itself needs to cancel or restructure the grant because of changing business conditions, shareholder revolt, or the design no longer works? The three grants in our sample were significantly modified after the fact, and each comes with its own optical risks. Investors notice when the goalposts move.

Shareholder backlash. Special stock awards are of primary interest to investors. Approximately 30% of companies that have failed pay votes in recent years have cited special awards as a key factor. GE's $57 million grant to Larry Culp contributed to the failure of the 2021 vote with 42 percent support. Paycom's $176 million grant had a similar impact. Coty's $146 million grant to Sue Nabi went against recommendations from both major proxy advisers. These are not special cases.

Another recommended set

For boards evaluating CEO mega-grants, the data supports a different set of questions than those typically asked.

- Reserve your instrument for authentic, transformative situations. Grants structured around a clear transformative mission delivered a median grant date value of 296% with an annualized alpha of 5.9 points. Daily retention and recognition use is significantly reduced.

- Combine market-based metrics with at least one operational anchor. In our sample, only 17% of grants do so. Pure price design provides minimal protection if the rally outpaces business fundamentals.

- Use a performance period of at least 5 years. The data directly supports this, with proxy advisors viewing expanded horizons favorably.

- Combine the grant with an explicit commitment that no additional grants will be required during that period.. This would address both dilution and the issue of “pay floors” that could lead to shareholder backlash if subsidies underperform, but it would tie the hands of current and future remuneration committees.

- Spend more time on succession and governance risks than on aligning goals. Performance design may work as intended. A more difficult question is whether CEOs and companies are positioned where boards expect them to be five to 10 years from now.

There is one further finding worth highlighting. That means the hurdles are significantly higher for small-cap companies. The S&P 600 mega-grants in our sample had a median realized value of zero, and companies underperformed their index by nearly 18 percentage points annually. Instruments that work reliably in the context of large-cap transformation have not transferred to down markets. Small-cap boards should either skip the mega-grant or invest significantly more in design discipline before proceeding.

Megagrants are a powerful tool. Used at the right time, with the right structure, and by the right board, this plan can deliver economic value to CEOs beyond what the grant date disclosure would suggest. And that tends to happen because the underlying companies truly outperform the shareholder market. When used in routine situations, or situations where the CEO is unlikely to remain for the duration, risk is concentrated where performance design cannot reach. The data argues for careful and infrequent use of this tool.