I was going to say “died,” but I thought that would give readers the wrong impression that I don't expect any more downturns. In fact, I don't think the word “cycle” is any more descriptive.

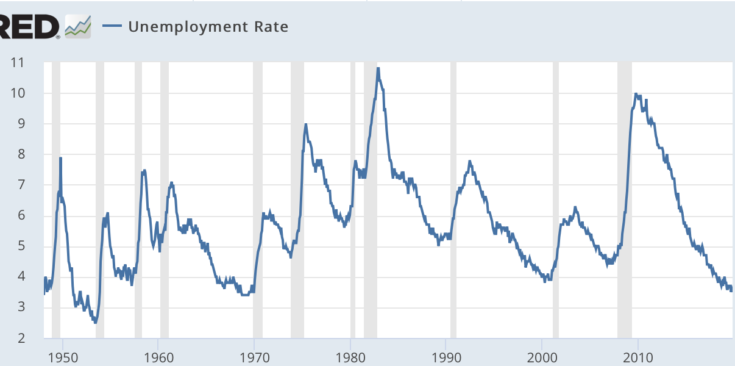

In November 1982, unemployment reached 10.8%, the highest since World War II. The United States had experienced eight recessions in the previous 37 years (and nine in the 38 years before that), and things seemed to be getting worse (the two worst were in 1974 and 1981-1982). No one expected the United States to experience only three recessions in the next 37 years. What went right?

After the war, monetary policy was influenced by a fairly simple Keynesian model. Problems in the 1970s and early 1980s led to “neo-Keynesianism”, a synthesis of Keynesianism and Monetarism, incorporating monetarist ideas such as the natural rate hypothesis and the importance of the Fisher effect, and also Keynesian ideas such as interest rate targeting and policy activism. The Taylor rule is a simple way to think about this synthesis.

As monetary policy has become more effective, recessions have become much less frequent. Importantly, this process is likely to continue. If we achieve the first soft landing in U.S. history over the next few years (as I expect), we should see only one recession over the next 37 years.

Economic experts have yet to fully understand the impact of improved monetary policy. Noah Smith:

It's impressive how the U.S. economy has held up over the past year. Leading indicators as early as 2018 suggested a growing risk of recession in 2019 or 2020. Then, earlier this year, the yield curve inverted, a traditional signal that a recession is imminent (it has since reversed, but this usually happens before growth actually turns negative). The trigger for the recession wouldn't be hard to pinpoint: a combination of a slowing China and President Donald Trump's trade war. Already, countries like Singapore and South Korea that export a lot of manufactured goods to China are slowing.

Yet despite all the ingredients for a recession, none is happening: the economy is in its longest expansion since the end of World War II and recently surpassed the long boom of the 1990s.

That's all pretty reasonable, but I see it a little differently. Smith is absolutely right that real shocks often “trigger” recessions — think of the 2007-2008 housing and banking crisis. But they Cause Recessions are triggered by tight monetary policy, which results in a sharp slowdown in NGDP growth. As monetary policy improves, real shocks become less and less likely to cause bad monetary policy and thus a recession. Real shocks become more likely to cause a slowdown in RGDP growth, as they did in 2015-2016.

However, the unemployment rate continued to fall from 2015 to 2016, so it was far from a recession. The United States has never even experienced a mini-recession in which the unemployment rate rose by 1.0% to 2.0% and then began to fall, and periods when the unemployment rate falls are fundamentally different from periods when the unemployment rate rises by 2.0% or more.

Just as the recessionary periods of the 1970s and early 1980s led to improvements in monetary policy, the Great Recession led to further improvements. The Fed now understands that the natural rate of interest is long-term declining. The last three recessions were caused in part by the Fed overestimating the natural rate and not cutting rates fast enough and deep enough to stop recessions when they started to get in trouble. The Fed is unlikely to make the same mistake in the future. The Fed also understands that in an environment of slowing NGDP growth, an inflationary shock like the one in 2007-2008 is not worth worrying about. It also understands that in recessions, it is necessary to commit to policies like level targeting. The only downside, of course, is that the Fed is more likely to face zero lower bound problems in the future.

The reduction from eight recessions to three over 37 years is not as impressive as it may seem. The percentage of periods with high unemployment has not fallen as dramatically as expected due to the slow economic recovery. However, a further reduction in recessions to one over the next 37 years would be a big step forward. It's going to be a really big problemThis means the Fed has learned how to achieve a soft landing and create a long period of near full employment.

Why am I optimistic that we are on the verge of achieving the Holy Grail of macroeconomics when we have never experienced a soft landing before? Other similar economies such as Australia and the UK have learned how to achieve soft landings, so I see no reason why recessions will not become increasingly rare in the US.

In the 38 years since World War II, recessions have occurred, on average, about every four years. They occurred just as frequently before World War II. If my prediction of only one recession in the next 37 years is correct, then the term “cycle” will no longer be appropriate. In that sense, economic “cycles” are disappearing.

At this point, this is a “tentative forecast” and assumes no recession in the next three years. If this soft landing occurs, it will change from a tentative forecast to a confident forecast. Of course, I won't live long enough to see if a 37-year prediction comes true, but I hope to live long enough to see if it does. Highly likely to happenIf a soft landing becomes a normal part of the US macroeconomy,